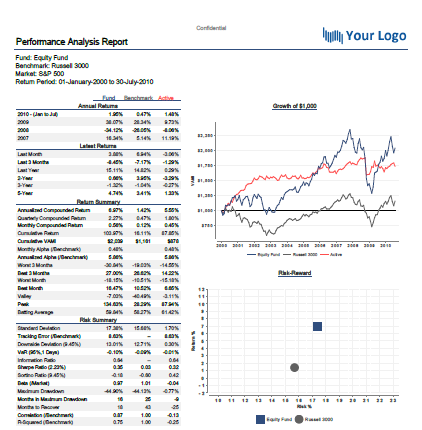

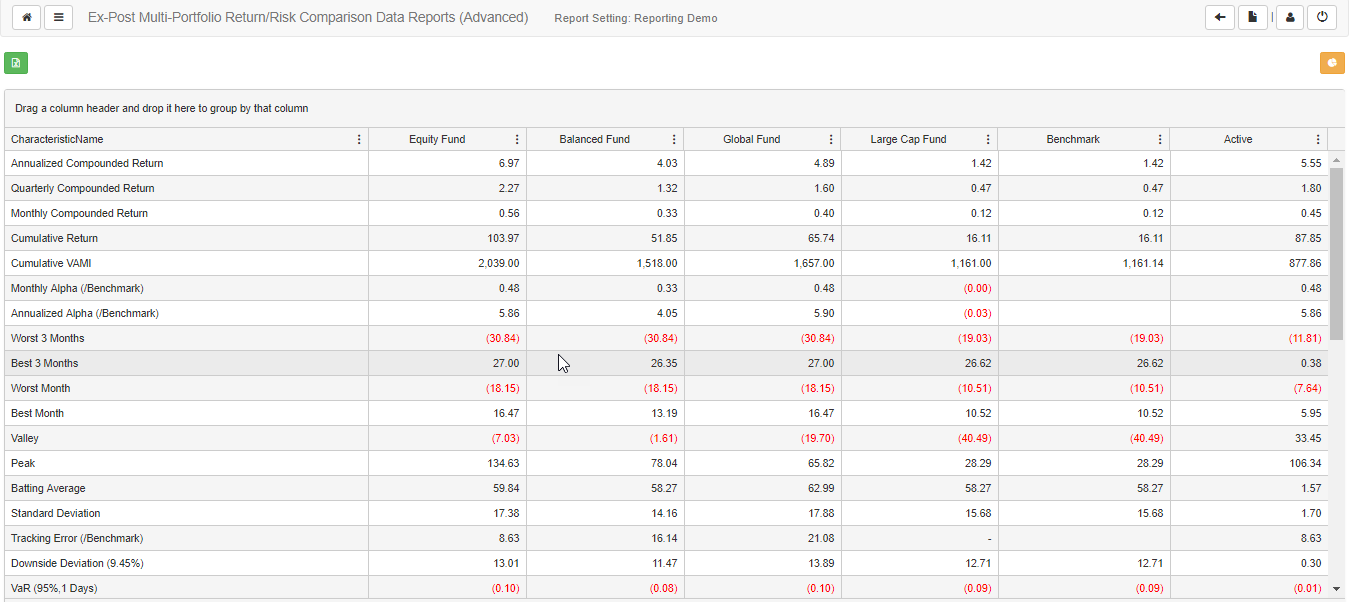

Return & Risk powered by SAYS

SAYS offers robust ex-post return and risk analytics for any frequency of portfolio and benchmark time series data. Performa may be deployed rapidly to provide users with on-demand analytics and reporting. Monitor performance over monthly periods, calendar years, and rolling periods, while also tracking risk statistics such as Sharpe Ratio, Tracking Error and VaR.

Regardless of the source and format of your portfolio data, SAYS can have your ex-post return and risk needs addressed rapidly.